Article by Sarah Reichling, John Toscano, Sarah Hintz, Connie Lira, Kyle Dawley, Ellen Mccabe, Scott Hess And Amy Bradley, CliftonLarsonAllen

In January, NBOA released a new guide, “Tax Compliance Considerations for Not-for-Profit Independent Schools.” Accountants at CliftonLarsonAllen have broken down essential concepts to enable business officers and controllers to assess their school’s tax compliance status, areas of greatest risk and associated mitigation steps.

The Bottom Line

- NBOA's new tax guide for independent schools provides details on key areas schools may have questions about.

- The guide shares common risk areas and strategies to mitigate them.

- Find detailed, visual explanations of Form 990 in the guide itself.

Although an independent school with tax-exempt status is not required to pay federal income taxes, it still may have other types of tax requirements. In addition to filing an annual information return with the Internal Revenue Service, most independent schools are required to file and pay payroll taxes and other state and local taxes. For some institutions, unrelated business income and foreign tax reporting may even become an issue. It is the responsibility of the independent school to provide transparent governance, financial and operational information to the Internal Revenue Service and the public in order to maintain tax-exempt status.

This guide is intended to support the finance role by covering the various complex tax issues an independent school may encounter.

The following is a brief excerpt of the 45-page publication. NBOA members can download the guide for free and nonmembers can purchase it at nboa.org/taxguide.

In a perfect world, independent schools would not only understand what their tax and compliance risks are but also have staff with specific tax and compliance expertise to manage each and every risk that arises. In reality, most schools struggle with determining risks, or lack sufficient resources to manage those risks, or cannot figure out where to start. Because of these real-world constraints, a practical approach is encouraged, as the aim is progress, not perfection.

- Designate the position in the business office that will take the lead in starting the compliance process. This person is usually the business officer or controller and does not need to be an expert. They should have an interest in furthering the ultimate goal of compliance — and the long-term vision to get there.

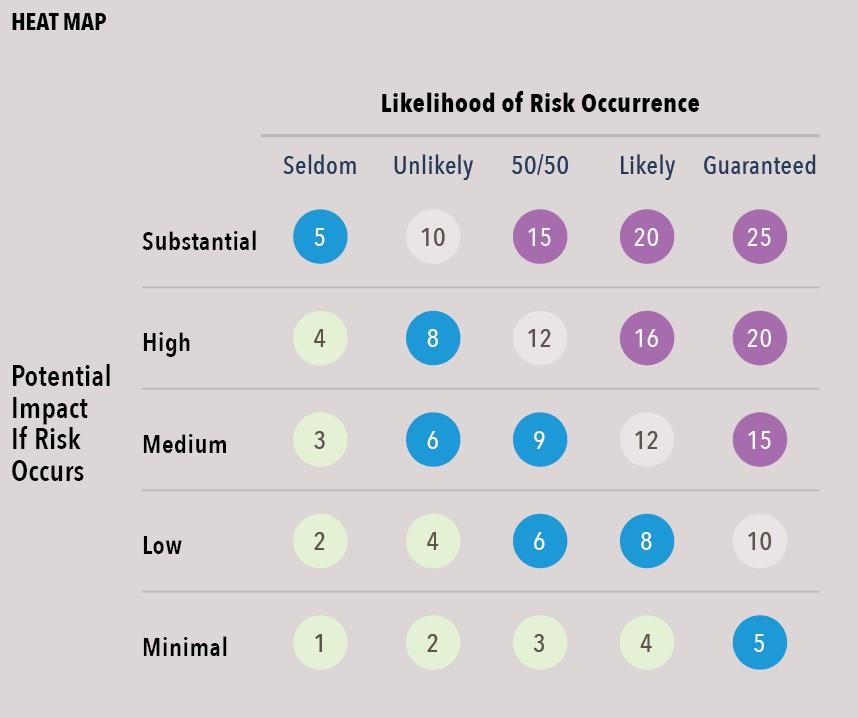

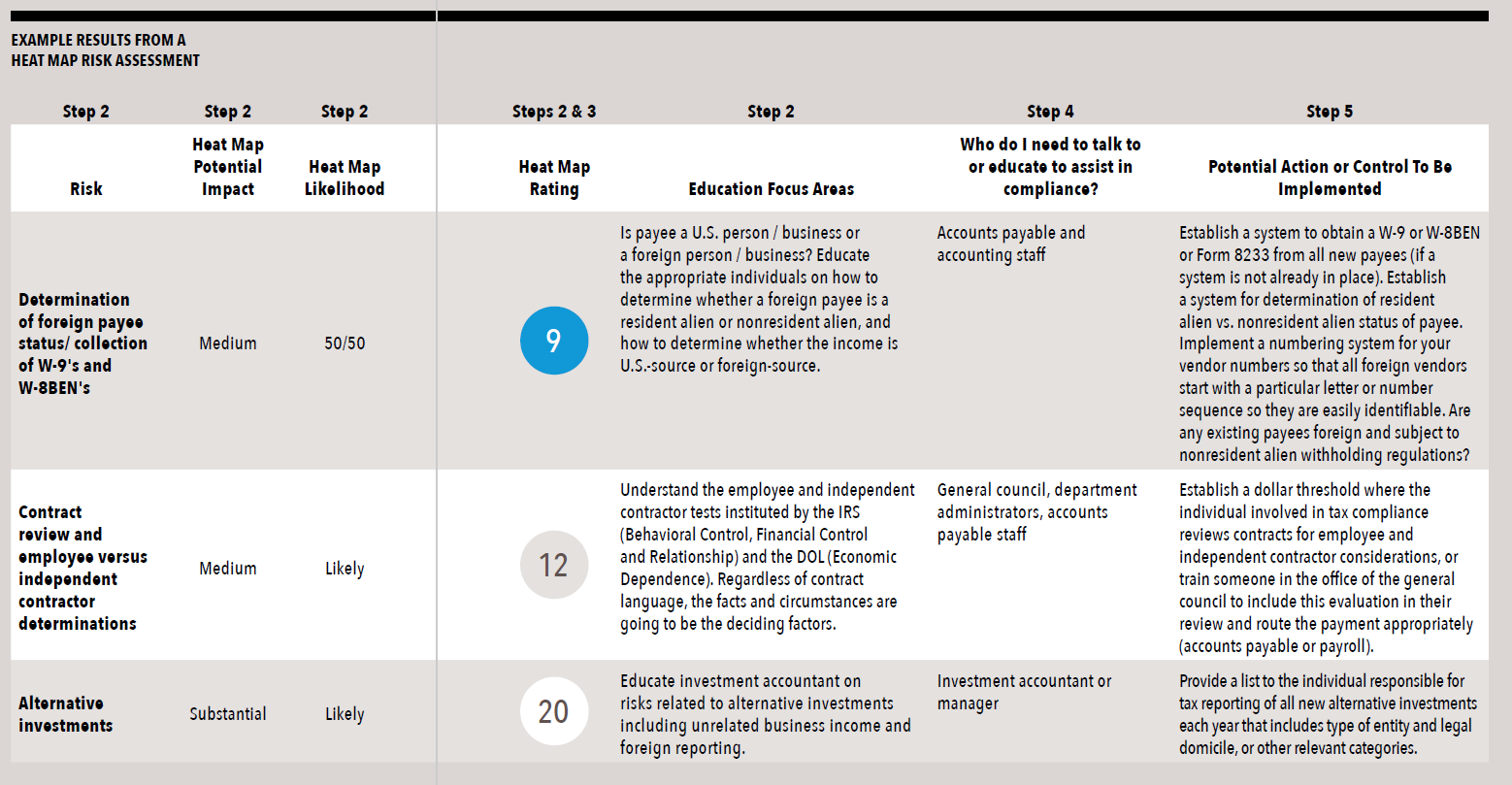

- Determine the potential tax risks to your school and use a heat map to rate these risks. Examples of potential risk areas are included on the previous page. Using a heat map creates a visual representation of the magnitude of each risk at your school.

- Determine what risk threshold the organization is comfortable with utilizing numbers and colors similar to the example below. The risks above this level are the risks that should be addressed first, in order of importance, based on the ranking from the heat map.

- Determine who within your organization needs to be involved in managing each risk. Achieving compliance requires a team effort. You aren’t looking for perfection or to create tax and compliance experts within your organization, but you do want to provide awareness and education among your staff within the business office and the leadership team so you have partners in achieving your compliance goals.

- Determine actions or controls that can be implemented in each risk area.

- Understand that you may need to be flexible. Managing these risks to achieve a level of compliance within your school’s risk thresholds — with the resources at hand — may require you think outside the box.

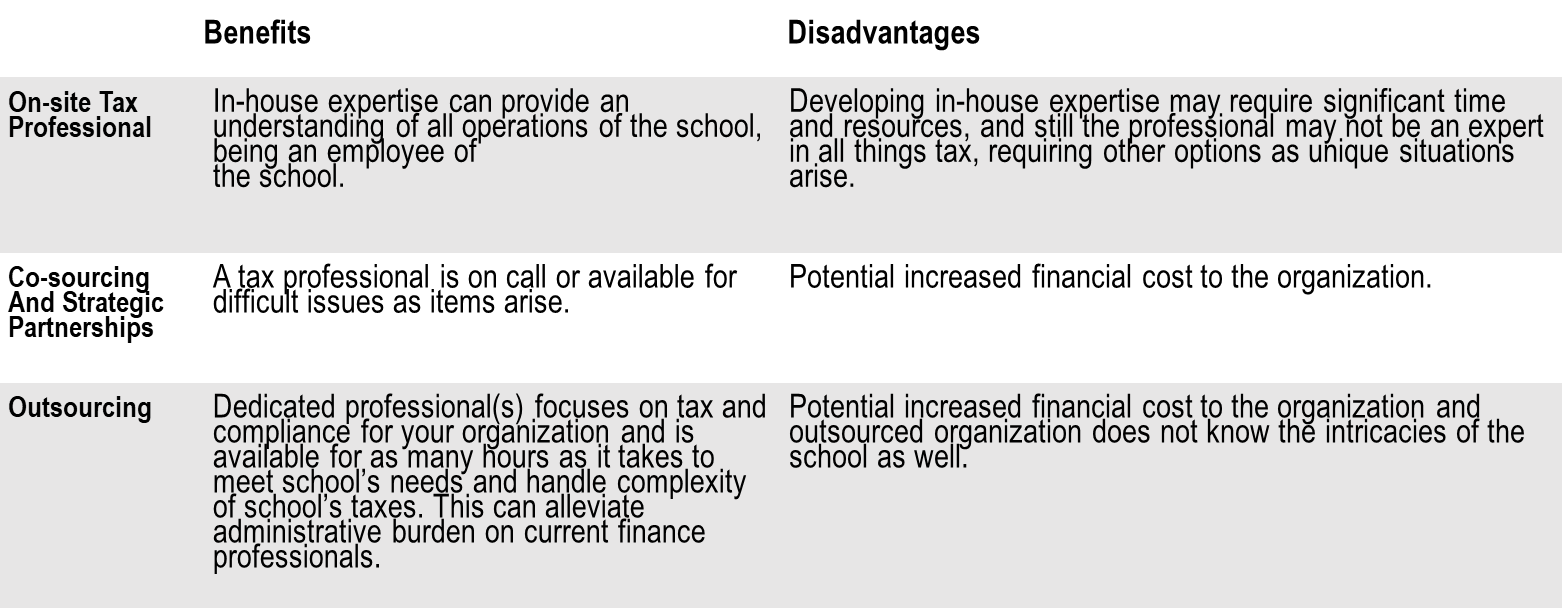

Tax and Compliance Models

Independent schools usually use one of three common tax and compliance models, depending on the complexity of the school’s compliance needs and structure of its finance department. One is not better than the other; your organization’s needs and vision will determine which is the most appropriate for your school. These models are explained in the chart to the right.

Maintaining Exemption

501(c)(3) public charities will want to do the following to maintain their tax-exempt status.

- File with the IRS annually. One of the following forms is required: Form 990, 990-EZ, or 990-N.

- Due 15th day of the 5th month after fiscal year end.

- For a six-month extension, use Form 8868.

- For example, with a fiscal year end of 6/30/20XX FYE, the initial due date would be 11/15/20XX, and the extended due date would be 5/15/20XX+1.

- If entity type is a trust, due dates are one month sooner.

- For example, the trust initial due date would be 10/15/20XX and the extended due date would be 4/15/20XX+1 extended.

- Follow public disclosure requirements. A copy of the following must be provided to anyone that asks:

- Annual IRS return — You can remove donor names and addresses from Schedule B.

- Annual Unrelated Business Income Return Form 990-T, if applicable.

- Original application for exempt status, Form 1023 — If the school applied for exemption before July 15, 1987, you only have to make it available if you still have a copy.

TIP: If the school applied after July 15, 1987 and doesn’t have a copy, a copy can be requested from the IRS.

- Follow donor receipting rules.

- If the school receives a payment of $75 or more, and a portion is contribution and a portion is exchange transaction, a donor receipt is required, and the school must estimate the FMV of exchange received in return for the payment.

- If a payment is all contribution, no donor receipt is required. Best practice, however, is to proactively provide a receipt to maintain good donor relations because the donor needs a receipt to take a tax deduction.

- Avoid the following transaction types:

- Private benefits: These transactions benefit a person or business outside the charitable class of the school.

- Private inurement: These are transactions with those in authority, their family, or businesses.

- Political transactions: These are taxable.

- Lobbying activities — Nonprofit organizations risk losing tax-exempt status if a substantial part of its activities is attempting to influence legislation.

- Excessive amounts of Unrelated Business Income (UBI) — Understand your revenue streams and whether activities are part of the exempt purpose or not.

- Keep up with payroll filings.

- Keep up with other information filings, for example, 1099s.

- Keep up with state registration requirements, including sales tax obligations and exclusions.

- Pay attention to (that is, don’t ignore) federal or state notices. Currently the IRS communicates primarily through paper mail, so ensure anything received by the IRS is reviewed and dealt with in a timely manner.

To track this, consider creating a central chart like the one below that appropriate staff members have access to: